Scotland's Growing Natural Capital Markets

Insights and Learning from the FIRNS Programme.

March 2025

A report written by Jack Scriven at AchieveGood in collaboration with Social Investment Scotland and NatureScot. For any enquiries, please contact:

Executive Summary

Scotland's natural capital markets present a significant opportunity to attract private investment for nature restoration while delivering environmental and community benefits. The Facility for Investment Ready Nature in Scotland (FIRNS) demonstrates how this potential can be realised by supporting innovative projects and market development.

Through providing £4.75 million in grant support across 35 projects, FIRNS has generated crucial insights, notably into four key aspects of market development: demand for ecosystem services, project pipeline development, business model innovation, and governance frameworks. The programme highlights both the challenges and opportunities in creating high-integrity markets that work for communities, landowners, and investors.

Early success in carbon markets, combined with emerging opportunities in biodiversity, natural flood management and water quality, shows growing potential for private investment in nature restoration. However, realising this potential requires continued support for project development, standardised approaches to reduce costs, and policy frameworks that ensure genuine environmental and social benefits.

These insights are informing Scotland's natural capital policy framework, supporting the country's ambitious climate, biodiversity, and just transition goals while building capacity for future market growth.

Acknowledgements

This report was produced by AchieveGood in collaboration with Social Investment Scotland and NatureScot's Natural Capital team drawing on evidence gathered throughout the FIRNS programme delivery.

The analysis draws on multiple sources, including FIRNS project documentation, Community of Practice surveys and discussions, stakeholder workshops, and market research. We are particularly grateful to the case study contributors who provided detailed insights into their projects:

- Fernanda White (Achnacarry Estate)

- Paul Sizeland (Fisheries Management Scotland)

- Simon Herko (Dreel Burn Project)

- Ed Heather-Hayes (Fife Coast and Countryside Trust)

- Peter Faccenda (Flow Country Partnership)

The report benefits from the active participation of the FIRNS Community of Practice members, whose willingness to share experiences and learning has been invaluable. Their contributions through surveys, discussions and workshops have provided crucial evidence of what works in practice.

Special thanks to all project teams who contributed data, participated in evaluation activities, and shared their insights to support market development in Scotland.

Introduction

The Facility for Investment Ready Nature in Scotland (FIRNS) represents a pioneering initiative to accelerate private investment in Scotland's nature restoration. A collaboration between The Scottish Government and NatureScot in partnership with The National Lottery Heritage Fund (NLHF), FIRNS aims to help create a pipeline of market-ready projects to attract responsible private investment in Scotland's nature.

Launched in February 2023, FIRNS has provided approximately £4.75 million in grant support across 35 projects, attracting significant interest with 99 Expressions of Interest across two funding rounds.

The programme operates through three interconnected workstreams:

- Grant funding for project development

- Gateway events supporting natural capital project development

- A Community of Practice facilitating knowledge sharing and collaboration

Supporting Investment Readiness through the Community of Practice

Central to FIRNS' success is its Community of Practice (CoP), facilitated by Social Investment Scotland (SIS). SIS brings significant expertise in social investment and enterprise development, complementing their wider role in Scotland's impact investment landscape.

The CoP supports projects through:

- A curated programme of events delivered in three blocks from May 2024 to April 2025

- Peer-to-peer learning and knowledge exchange

- Access to specialist expertise and resources

- Regular sharing of project experiences and best practices

- Online collaboration through a dedicated digital platform

By November 2024, the CoP had grown to include up to 62 active members across 37 projects, creating a vibrant community that extends beyond FIRNS-funded projects to include graduates of the Investment Ready Nature Scotland (IRNS) programme and the Riverwoods Investment Readiness Pioneers. The forum functions as a vital source of information for Scottish Government and NatureScot to understand emerging challenges and opportunities in natural capital markets, helping inform policy development and identify where additional support may be needed.

Policy Context

FIRNS operates within Scotland's defined natural capital policy framework, which emphasises responsible, values-led investment aligned with key national priorities:

- Net Zero Targets: Supporting Scotland's commitment to reach net-zero emissions by 2045

- Biodiversity Goals: Contributing to halting biodiversity loss by 2030 and restoring nature by 2045

- Just Transition: Ensuring benefits are shared equitably with local communities

- Marine Protection: Supporting goals to protect 30% of Scotland's seas by 2030

The recently published Natural Capital Market Framework outlines seven key interventions planned by 2026 to increase high-integrity investment, providing strategic direction for market development while emphasising community benefit and equitable access as core principles.

Insights and Learning and Updates from the FIRNS Programme

Drawing from the experiences of FIRNS projects and extensive stakeholder engagement, this report examines critical aspects of Scotland's emerging natural capital markets:

- Demand: Explores current and emerging markets for ecosystem services, buyer preferences, and mechanisms to strengthen market demand.

- Pipeline: Analyses the development of Scotland's natural capital project pipeline, examining barriers and opportunities for scaling investment-ready projects.

- Business Models: Investigates approaches to creating sustainable revenue streams and viable financial structures for natural capital projects.

- Legal Structures, Governance and Community Benefits: Examines frameworks for ensuring projects deliver genuine environmental and social benefits while remaining commercially viable while managing risks.

Each section combines analysis of FIRNS project experiences with case studies demonstrating practical implementation. The aim is to share learning and inform future policy development while providing practical insights for project developers, investors, and other stakeholders in Scotland's natural capital markets.

Demand for Ecosystem Services in Scotland

Overview of Demand in Scotland

Scotland's natural capital markets are evolving rapidly, with some more established revenue streams alongside emerging opportunities. Understanding the current buyer landscape is crucial for projects seeking to monetise ecosystem services. The market encompasses both limited compliance-driven demand and voluntary commitments, with varying levels of maturity across different environmental outcomes.

Active Markets

The most established markets in Scotland centre around carbon sequestration through the Woodland Carbon Code (WCC) and Peatland Code (PC). These verified schemes provide a framework for projects to generate carbon credits that can be sold to organisations seeking to offset their emissions. The global market for carbon credits reached £1.3 billion in 2022 (Paying for Quality (2023) Ecosystem Marketplace Insights Report) with forecasts suggesting potential growth to £1 trillion by 2037 with appropriate regulatory frameworks (Carbon Offset Market could reach £1 Trillion with right rules.)

The Woodland Carbon Code has seen steady growth in both volume and price. Recent data shows average prices increasing from £14.93 per Pending Issuance Unit (PIU) in 2021 to £25.36 in 2023 (UK Carbon Price Index) demonstrating growing market confidence. The Peatland Code, while newer, is also gaining traction, with recent trades averaging £23.95 per PIU (UK Carbon Price Index).

Emerging Markets

Several new markets are developing beyond carbon sequestration. These include:

- Biodiversity credits and ecosystem health metrics

- Water quality improvements and natural flood management

- Marine and coastal ecosystem services

- Integrated landscape-scale restoration projects encompassing multiple markets

While these markets are still nascent, growing corporate requirements around environmental disclosure and increasing awareness of nature-related risks are driving interest in developing standardised approaches to measuring and valuing these benefits.

Current Buyer Landscape and Motivations

Several key factors are driving the market for nature-based solutions:

- Growing corporate requirements around environmental disclosure particularly through frameworks like the Taskforce on Nature-related Financial Disclosures (TNFD), and managing nature-related risks.

- Large institutional asset managers demonstrating increasing interest in natural capital strategies, with major firms like Abrdn, HSBC, Gresham House, and BlackRock developing dedicated investment funds.

- Government support through policies and commitments, such as the Scottish Government's target to restore 250,000 hectares of peatland by 2030

- Technological advancements enabling better monitoring and verification of outcomes

However, the market remains predominantly voluntary rather than compliance-driven, with demand currently influenced by corporate social responsibility and environmental commitments rather than regulatory requirements, and it is currently developing slower than some early predictions, as can be seen with carbon prices: NEW! State of the Voluntary Carbon Markets 2023 finds VCM demand concentrating around pricier, high-integrity credits.

Perspectives from FIRNS Projects

Drawing on feedback from FIRNS projects at the November 2024 Community of Practice event and ongoing project evaluations, several key themes emerge around market demand and buyer preferences.

Demand

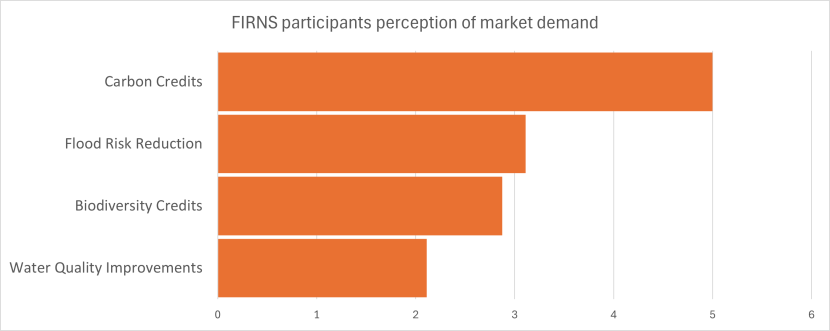

A survey of FIRNS projects in November 2024 provides quantitative insights into current market demand from project experiences. Projects were asked to rate current buyer demand across different ecosystem services on a scale of 1-10: overall, carbon was seen to be the most in demand at 5, and overall demand was not seen as strong.

Figure 1: FIRNS Project participants perceptions of market demand for carbon credits, flood risk reduction, biodiversity credits and water quality improvements.

Click for a full description

Carbon Credits: 5

Flood Risk Reduction: 3.1 approx

Biodiversity Credits: 2.9 approx

Water Quality Improvements: 2.1 approx

Quality vs Price Considerations

FIRNS projects report mixed feedback on buyers' willingness to pay premiums for high-integrity credits with strong co-benefits, with survey data showing a moderate average rating of 6 out of 10. While buyers express interest in local projects with demonstrable community benefits, price sensitivity remains a key factor. Notably, even when providing anonymous feedback, buyers show reluctance to commit to specific price points for premium credits, suggesting a gap between expressed interest and willingness to pay in this developing market.

Biodiversity and Ecosystem Health

There is emerging interest in biodiversity credits and broader ecosystem health measures, but the market remains at an early stage. Projects report that potential buyers are awaiting greater clarity on how voluntary biodiversity credits will align with upcoming reporting requirements like TNFD. Several FIRNS projects suggest demand exists for something similar to England's Biodiversity Net Gain system, indicating the appetite for a more structured compliance-based approach.

Geographic and Scale Considerations

A notable trend is buyers' preference for "offsetting on their doorstep" - investing in local natural capital projects. However, this creates challenges for projects in remote areas where there are fewer large corporate buyers. The disconnect between areas of high natural capital potential and locations of potential buyers remains a key market challenge.

Market Development Challenges

Projects consistently highlight several barriers to market development:

- The long timeframes involved in natural capital projects (20-50 years) create uncertainty for buyers in committing to future purchases

- Accessing buyers directly can be challenging as many are "firewalled" by brokers

- There is significant apprehension around market stability and long-term demand

- Many potential buyers struggle to quantify their current environmental impact, making it difficult to determine their future offsetting needs

The Achnacarry Estate Case Study

The Achnacarry Estate case study illustrates key themes in market demand and buyer preferences. As a large-scale landscape restoration project engaging with buyers, it provides valuable insights into investor requirements, carbon credit pricing, and the challenges of securing of securing finance.

Case Study: Achnacarry Estate – Arkaig Natural Capital Project

Achnacarry Estate, located north of Fort William, is undertaking an ambitious landscape-scale restoration project around Loch Arkaig. The estate encompasses multiple mountains and glens, with plans to restore ancient woodlands, expand native woodland cover, and deliver peatland restoration across the catchment. Having already completed three phases of peatland restoration across nearly 400 hectares, the project is now seeking private investment to accelerate and scale up its nature restoration work.

The project stands out for its scale and landscape-level approach, combining:

- Native woodland creation through planting and natural regeneration with natural regeneration preferred where seed sources exist

- Peatland restoration at the top of the catchment

- Holistic nature recovery, including tackling invasive species and managing deer populations

- Partnership working with neighbours through the Loch Arkaig Landscape Restoration Partnership And Beò Arceig

Investment Journey and Lessons Learned

The project's significant scale and single ownership has made it attractive to potential investors, with multiple parties expressing interest. The estate has been able to present a clear vision for landscape-scale restoration, demonstrating both the current state and future potential when showing investors the site. However, this scale also brings challenges - particularly around securing sufficient grant funding and managing delivery timelines.

Carbon Credit Demand

Key insights on buyer preferences include:

- A strong focus on pre-2050 carbon credits, with earlier vintages commanding higher values

- Clear preference for woodland carbon over peatland credits, partly due to uncertainty around SBTI guidance

- Interest in co-benefits and high integrity credits, but only as additions to carbon value rather than standalone products

- Sensitivity around price despite recognition of quality and co-benefits

Deal Structure

The project has explored various investment models:

- Direct offtake agreements with end buyers: Contracts where buyers commit to purchase carbon credits directly from the project at agreed prices, providing revenue certainty while the estate retains control over implementation.

- Leasing models with third-party investors: Arrangements where investors provide upfront capital and manage the project in exchange for a share of carbon credits or revenue over an extended period.

- Special Purpose Vehicle (SPV) structures Creation of separate legal entities specifically to develop and manage the restoration project, often involving multiple investors and complex governance arrangements.

The team ultimately favoured pursuing direct offtake agreements as :these offered greater certainty on pricing and carbon unit commitments while maintaining estate control over delivery and future sales. This approach also proved simpler than alternative structures requiring SPVs or complex sharing arrangements.

Key Challenges

Several significant barriers emerged during the investment journey:

- Uncertainty around forestry grant funding levels making it difficult to determine the investment gap

- Variable and often lengthy statutory approval processes affecting delivery timelines

- High upfront costs for project development, including surveys and stakeholder engagement

- Complexity of balancing investor requirements for guaranteed carbon volumes against delivery risks

Learning Points

©Hazel Boyd

- Investment readiness and development costs

- Significant upfront investment is required to reach a stage where projects can meaningfully engage with investors

- Project development costs increase with scale but are essential for creating investable propositions

- FIRNS funding was crucial in supporting detailed financial modelling and investor engagement

- Buyer and investor preferences

- Pre-2050 carbon credits can be attractive to some, although not to all, depending on the timeframe of their commitments.

- Woodland carbon is preferred over peatland credits due to focus on removing carbon rather than preventing emissions and clearer measurement

- Co-benefits enhance appeal and can lead to price premium but may not be of the scale to cover project costs without grant support

- Direct engagement with end buyers can be more effective than working through intermediaries, especially for larger scale projects like Achnacarry where costs are reduced. However, it is important to note they can also play a useful role in aggregations, connectivity and taking on some elements of risk.

- Grant funding certainty

- Uncertainty around forestry grant levels makes it difficult to define the investment gap and develop business cases

- Current grant structures can work against landscape-scale projects as rates reduce for larger areas

- Blended finance remains essential - even with private investment, many projects still require grant support to be viable, especially to support early development and baselining.

- Project delivery risks

- Variable timelines for statutory approvals create uncertainty around carbon credit delivery dates

- Projects need to balance maintaining sufficient risk buffers against making attractive investment returns

- Insurance products are limited and expensive, focused more on buyers than project developers

- Managing community and stakeholder relationships requires significant time and resource

- Business model development

- Simpler structures like direct offtake agreements can be preferable to more complex Special Purpose Vehicle (SPV) arrangements although there can be use cases and advantages for both.

- Models need to carefully balance investor certainty with realistic delivery capabilities

- The timing of carbon credit verification and sales significantly impacts financial viability

- Scale brings both opportunities and challenges for investment structures

Demand: What Would Help

Drawing from FIRNS project feedback and market analysis, the following priorities would help accelerate private investment in nature restoration:

Market Framework and Standards

- Provide clear policy guidance on carbon and biodiversity credits, for example, by working SBTI requirements to clarify the role of different credit types, such as Peatland, providing guidance to buyers, and clarifying and ideally mandating Biodiversity net Gain mechanisms in Scotland.

- Support the development of standardised contracts and approaches to reduce transaction costs (as is being supported by a current FIRNS project)

- Consider mechanisms like price floors, offtake agreements or outcome-linked payments, such as contributing to maintenance costs, to increase market confidence and earlier buyer commitment

Grant and Planning Reform

- Provide greater clarity on available grant funding levels to enable business planning

- Streamline approval processes for larger landscape-scale projects

- Review grant structures that currently discourage larger projects

- Create more predictable timelines for statutory consent

Project Development Support

- Maintain support for early-stage project development to bridge the investment readiness gap

- Help projects engage effectively with buyers and investors

- Enable projects to gather robust baseline data and demonstrate outcomes

These targeted interventions would help address key barriers while maintaining environmental integrity and supporting the development of high-integrity natural capital markets in Scotland.

The Pipeline of Natural Capital Projects in Scotland

Overview of Natural Capital Opportunities in Scotland

Scotland's unique landscapes and environmental assets hold great potential for nature-based solutions, from peatland restoration to woodland creation and marine conservation. The development of a robust project pipeline is crucial to realising this potential and attracting consistent private investment to support Scotland's climate and biodiversity goals.

While market demand for ecosystem services increases, developing a pipeline of projects that can service this demand is crucial to market establishment. The nature and scale of buyer requirements directly influence which projects can progress to investment readiness, with implications for geographic distribution, project size, and development timelines.

The pipeline of natural capital projects in Scotland is currently characterised by high interest from investors and buyers but varying levels of development and investment. Analysis from the Investment Ready Nature Scotland (IRNS) and FIRNS programmes indicates that many projects are in the early to mid-stages of development, with the highest concentration of activity focused on developing business cases and financial models. It is worth noting that FIRNS has focused on supporting innovation projects and emerging revenue streams and provided less support to more established carbon projects; therefore, this analysis is not representative of the Scottish market overall.

Landscape and Ecosystem Projects

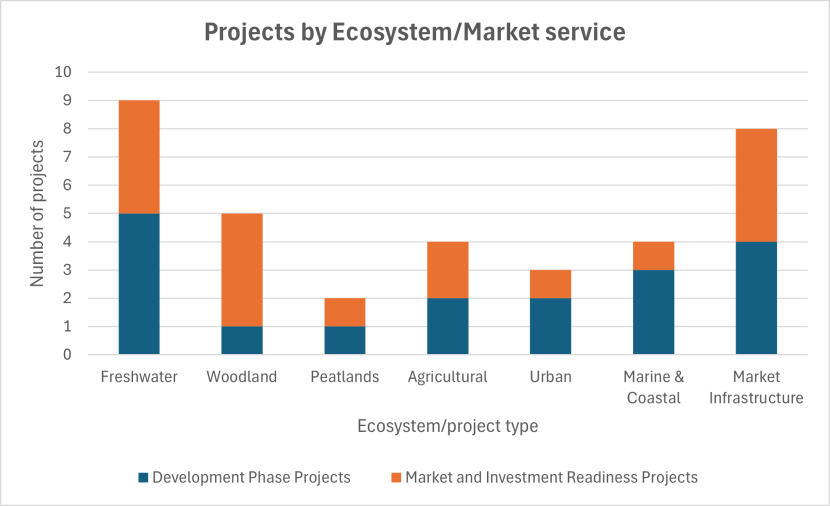

The FIRNS programme has supported projects across Scotland's key ecosystems, reflecting the diverse opportunities for nature restoration:

Peatland (2 projects, 6% of FIRNS portfolio)

- Scotland has over 2 million hectares of peatlands

- Approximately 75% are in degraded condition, emitting rather than storing carbon

- Represents 20% of Scotland's land area with restoration potential of up to 600,000 hectares: Peatland ACTION – restoring Scotland’s peatlands

Woodland (5 projects, 14% of FIRNS portfolio)

- Current woodland cover is 18% compared to European average of 38%

- Potential for native woodland expansion of up to 3.9 million hectares in upland areas

- Could deliver carbon removal of 6.96 million tons CO2 annually

Freshwater (9 projects, 26% of FIRNS portfolio)

- Over 125,000 km of rivers and streams

- Approximately 220 lochs designated as Sites of Special Scientific Interest

- Significant opportunities for natural flood management and water quality improvement

Marine & Coastal (4 projects, 11% of FIRNS portfolio)

- Over 18,000 km of coastline

- 462,000 square kilometres of sea area

- Extensive restoration potential in saltmarsh, seagrass and kelp forests

Agricultural (4 projects, 11% of FIRNS portfolio)

- Agricultural land covers approximately 75% of Scotland

- Significant opportunities for integrated land management and nature-friendly farming

Urban (3 projects, 9% of FIRNS portfolio)

- Over 80% of Scotland's population lives in urban areas

- Growing focus on green infrastructure and nature-based solutions for climate resilience

Market Infrastructure Development (8 projects,23% of the portfolio)

These projects focus on developing crucial market infrastructure, which in many cases, can attract investment and scale internationally:

- Development of new standards and codes

- Creation of aggregation mechanisms

- Establishment of trading platforms

- Community benefit frameworks

- Legal and contractual templates

This split between place-based landscape projects (77%) and market infrastructure (23%) reflects the dual need to develop both investable projects and the supporting mechanisms that enable market development and support investment.

Figure 2: FIRNS projects by ecosystem/market service including freshwater, woodland, peatlands, agricultural, urban, marine and coastal and market infrastructure.

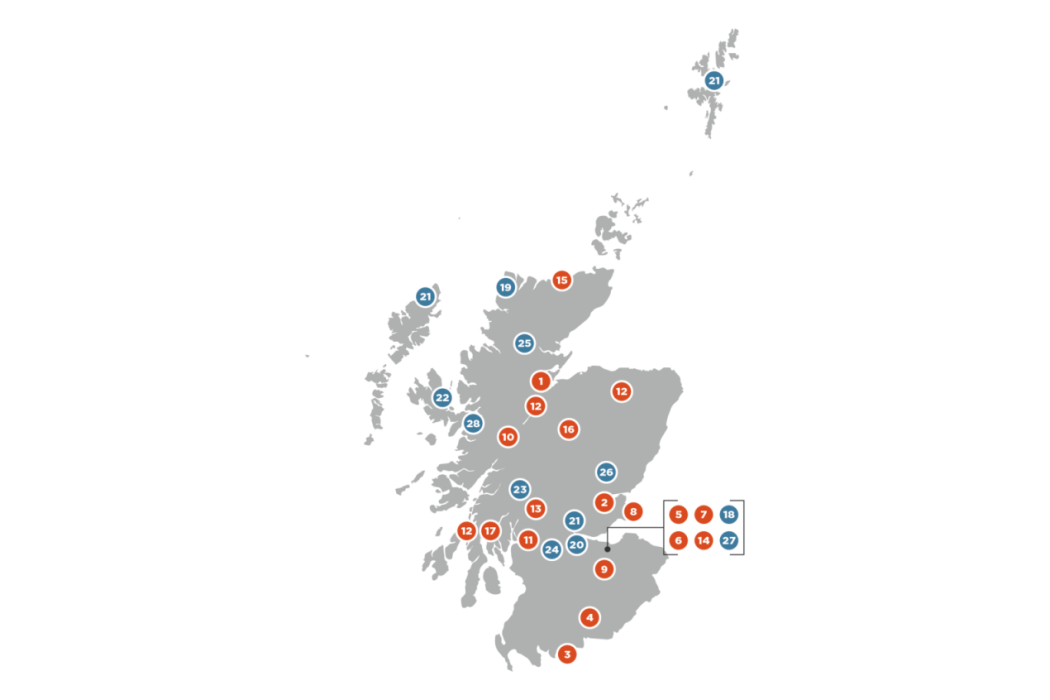

Geographic Distribution

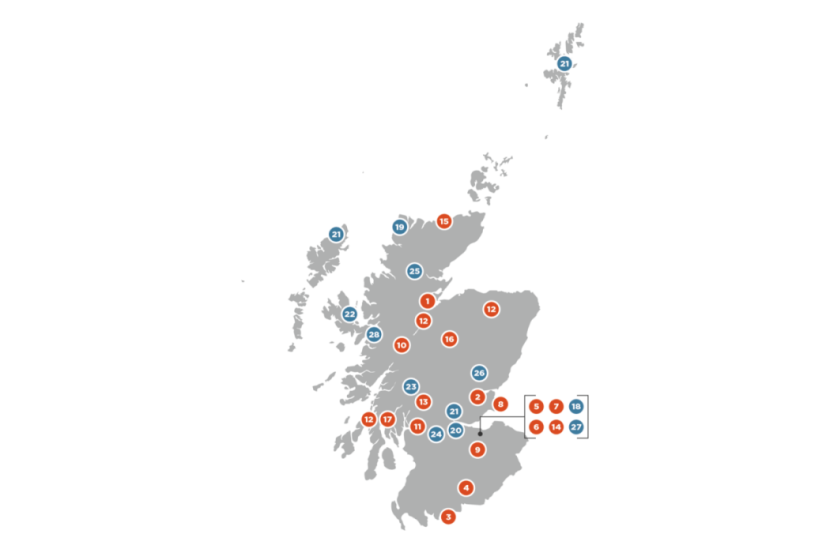

The geographic spread of projects demonstrates nationwide potential for nature restoration, with activities ranging from Shetland, down to Edinburgh and the Solway Firth.

However, there are notable variations in pipeline maturity across regions, often correlating with existing capacity and expertise in natural capital project development. Rural and more remote areas, in particular, face distinct challenges in developing projects to investment readiness and connecting with buyers, although they often hold some of the greatest potential for nature restoration.

Figure 4: FIRNS Place-based projects locations in Scotland including market and investment readiness projects (orange tabs) and those in a development phase (blue tabs).

Click for a full description

View a larger image of this map.

List of FIRNS Round 1 and 2 Projects

Market and Investment Readiness

1. Community Benefits Certification Mark for UK Natural Capital Projects, made by the nature finance certification alliance

2. Improved governance mechanisms for whole-farm and farm cluster natural capital project implementation

3. Solway Coast and Marine Project

4. Annan Riparian Restoration Network

5. Edinburgh New Gardens - Urban Nature Restoration Investment Scheme

6. Project L•AND

7. Buyer-seller contracts for carbon and other nature markets

8. Dreel Burn Investment Readiness

9. Financing Natural Flood Management for communities and wildlife of the Eddleston Water

10. Arkaig Natural Capital: Regenerative Investment in West Lochaber

11. Leven Landscape Enterprise Network (LENs)

12. Joint venture for Scaleable Community Benefits from Rewilding

13. Loch Lomond and the Trossachs National Park nature Finance Platform

14. Biodiversity crediting for woodlands, peatlands and other ecosystems

15. Flow Country Green Finance Initiative

16. Make Rewilding Your Business (MRYB)

17. Saving Scotland’s Rainforest with Natural Capital Finance

Development Phase

18. Scottish nature Impact Fund Feasibility Study

19. It’s in our Nature: Place Powered Futures

20. Advancing the UK Saltmarsh Code in Scotland

21. Unlocking the restoration of degraded peatland on crofting and common grazing land

22. Enabling Markets for Marine Natural Capital

23. Planning the Financial Future for Wild Strathfillan

24. Central Scotland Green Network Routemap to Green Finance Mobilisation

25. River Catchment Restoration Pilot at Alladale Wilderness Reserve

26. Braes of Alyth: Wild Cores and Corridors

27. Developing a sustainable Scottish source to sea, green finance model

28. The Knoydart Credit - A Partnership of Nature and Community

FIRNS Investment Readiness Progress

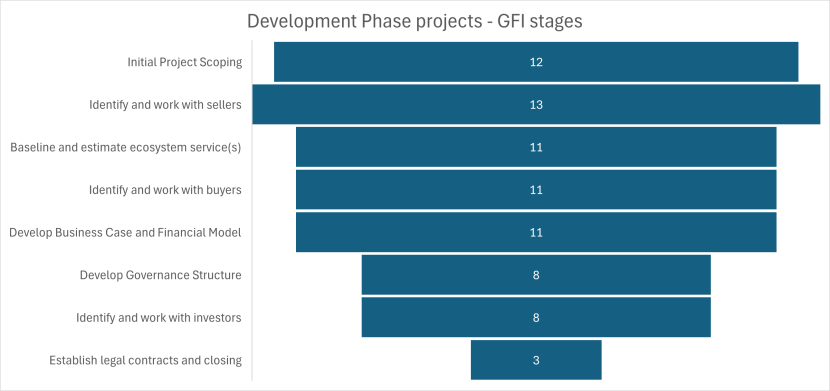

FIRNS projects used the Green Finance Institute's Investment Readiness Toolkit to track their progress towards investment readiness. The toolkit breaks down the project development process into eight progressive stages, from initial project scoping to establishing legal contracts and closing investments.

Development Phase projects as expected mostly covered the early stages of the toolkit:

- Initial Project Scoping

- Identifying and Working with Sellers

- Baselining and Estimating Ecosystem Services

- Identifying and Working with Buyers

- Developing Business Cases and Financial Models

Common challenges were reported across all stages; the most significant challenge was identifying and working with buyers, particularly around securing buying intent. Projects also reported challenges with community engagement, particularly defining specific community benefits, and with business case development, cashflow projections and selling strategies - a key pilar of the FIRNS programme and Community of Practice was supporting projects with these challenges.

Market and Investment Readiness projects are typically working across the later stages of the toolkit:

- Developing Business Cases and Financial Models

- Developing Governance Structures

- Identifying and Working with Investors

- Establishing Legal Contracts and Closing

These projects report fewer major delays overall but continue to face challenges around buyer and seller engagement and developing robust business cases. In contrast to Development Phase projects, they report more positive progress on community engagement but highlight new challenges around investor engagement, particularly identification and approach strategies.

This analysis indicates that while projects are making progress along the investment readiness journey, significant support is still needed to help projects transition through the later stages of development towards investment readiness. The data suggests that many projects are earlier in their investment readiness journey than initially anticipated at the outset of the FIRNS programme.

Figure 5a: FIRNS projects by Phase and GFI stage development, showing progress between Phases for Development Phase projects

Click for a full description

Development Phase projects - GFI stages

- Initial Project Scoping: 12

- Identify and work with sellers: 13

- Baseline and estimate ecosystem service(s): 11

- Identify and work with buyer: 11

- DevelopBusiness Case and Financial Model: 11

- Develop Governance Structure: 8

- Identify and work with investors: 8

- Establish legal contracts and closing: 3

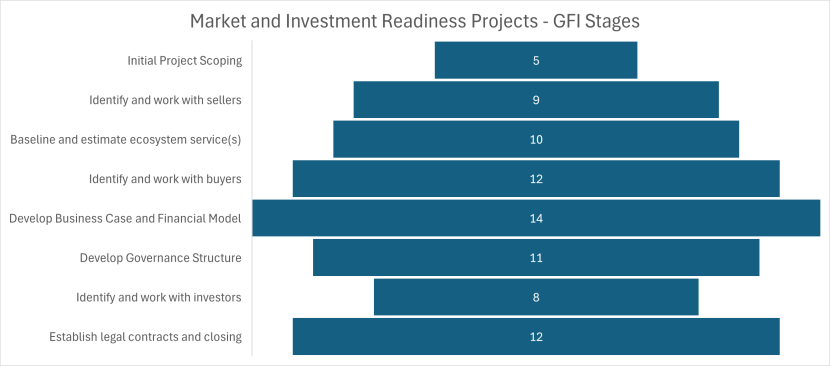

Figure 5b: FIRNS projects by Phase and GFI stage development, showing progress between Phases for Market and Investment Readiness Projects - GFI Stages

Click for a full description

Market and Investment Readiness Projects - GFI Stages

- Initial Project Scoping: 5

- Identify and work with sellers: 9

- Baseline and estimate ecosystem service(s): 10

- Identify and work with buyer: 12

- Develop Buiness Case and Financial Model: 14

- Develop Governance Structure: 11

- Identify and work with investors: 8

- Establish legal contracts and closing: 12

Perspectives from FIRNS Projects

The FIRNS Community of Practice provides valuable insights into what's working and what isn't in developing Scotland's natural capital projects. Based on our November 2024 event discussions and survey data, clear patterns are emerging.

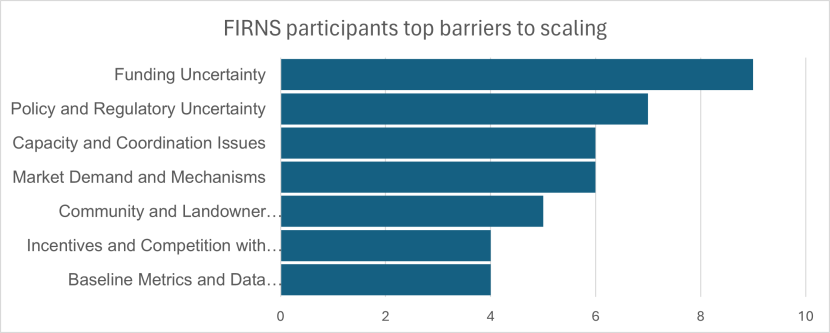

Key Challenges in Pipeline Project Development

Survey data from FIRNS projects highlighted several significant barriers to scaling projects, with funding uncertainty being the most frequently cited challenge (mentioned by 9 respondents). Policy and regulatory uncertainty was identified as the second most common barrier, followed by capacity issues and market mechanism challenges.

The main barriers identified were:

- Funding Uncertainty: Projects report difficulties in securing early-stage development funding and uncertainty around blended finance approaches

- Policy and Regulatory Framework: Lack of clarity on future agricultural payments and nature markets regulation

- Market Development: Limited buyer demand and uncertainty around emerging markets

- Capacity and Coordination: Limited expertise and resources, particularly in rural areas

- Baseline Data: Challenges in collecting and verifying 'decision-grade' data

- Community and Landowner Engagement: Complex stakeholder relationships and benefit sharing arrangements

Figure 6

Click for a full description

FIRNS Participant Survey perspectives on barriers to scaling including funding uncertainty, policy and regulatory uncertainty, capacity and coordination, market demand and mechanisms, community and landowner, incentives and competition and baseline metrics and dataeline metrics and data.

Funding Uncertainty: 9

Policy and Regulatory Uncertainty: 7

Capacity and Coordination Issues: 6

Market Demand and Mechanisms: 6

Community and Landowner: 5

Incentives and Competition with...: 4

BAseline Metrics and Data: 4

Progress on Scaling Projects

Feedback from FIRNS projects has highlighted that while there is significant potential for scaling projects, several factors are limiting progress:

- Landowner Hesitancy: Many landowners are adopting a "wait and see" approach due to ongoing agricultural reforms and broader market developments. There are concerns that future government grants may cover similar activities, or that current actions could negatively impact future revenue streams.

- Investment Readiness: Many projects require longer timescales than anticipated to reach investment readiness, with challenges around developing business cases and engaging buyers.

- Market Maturity: The early stage of markets beyond woodland and peatland carbon and variability in forecasted future carbon prices creates uncertainty around future revenue streams.

Aggregation Approaches

Project participants have revealed a growing interest in aggregation models to help achieve scale, with several approaches being tested:

- Geographic clustering of smaller projects

- Collaborative approaches through Regional Land Use Partnerships

- Development of standardised approaches to reduce transaction costs

- Creation of investment platforms to pool projects

- Implementation of Landscape Enterprise Networks (LENS), which connect businesses dependent on the same landscape assets with land managers who can deliver improvements through coordinated investments based on shared commercial interests

However, projects noted that aggregation brings its own challenges around governance, benefit sharing, and maintaining local engagement.

Landowner Engagement

Feedback highlighted the complexity of landowner engagement, with several key themes emerging:

- Importance of including public, private and community sectors (rated 10/10 in importance by survey respondents)

- Value of standardised approaches to measuring social impact (rated 10/10)

- Need for long-term certainty in legislation (rated 9/10)

Supporting Pipeline Development

Survey responses indicated strong support for additional mechanisms to support pipeline development:

- High value placed on the FIRNS Community of Practice for knowledge sharing (rated 8/10)

- Interest in a 'nature accelerator' providing further support (rated 7/10)

- Mixed views on the value of a centralised project catalogue (rated 6/10)

These perspectives highlight both the significant potential for scaling Scotland's natural capital project pipeline and the need for continued support to overcome current barriers. The strong emphasis on legislative certainty and standardised approaches suggests that policy framework development can play catalytic role in future pipeline growth.

The Fisheries Management Scotland Case Study

The Fisheries Management Scotland case demonstrates innovative approaches to pipeline development at catchment scale. It showcases how aggregation can address scale challenges while highlighting the complexities of coordinating multiple stakeholders and interventions.

Case Study: Developing a Scottish Source to Sea Nature Finance Model and River Catchment Restoration Portfolio Project

Fisheries Management Scotland (FMS) has completed one FIRNS-supported project exploring catchment-scale river restoration finance models. The current "River Catchment Restoration Portfolio Project" builds on this, aiming to develop a pipeline of investable projects across Scotland's rivers by leveraging 1,300+ actions identified in existing catchment management plans.

The project includes c50 delivery-ready projects and over 250 projects needing further development, covering interventions like peatland restoration, buffer zones, and tree planting. FMS is designing a fund structure with public sector backing, ethical oversight, and market-aligned funding portfolios to enable investment.

Project Development Challenges

- High costs for specialist assessments and engineering consultancy

- Complex landowner negotiations and agreements

- Navigating multiple stakeholder dependencies

- Accounting for competing land uses and agricultural subsidy interactions

A key challenge is developing a standardised monitoring framework that coherently reports outcomes across diverse projects and interventions. FMS is working to align this with the emerging Scottish biodiversity metric.

Project successes

- Completed initial Fund Design project establishing a foundation

- Developed and developing a substantial pipeline of delivery-ready and in-development projects

- Designed fund structure to enable responsible investment

Looking ahead

Near-term priorities include securing a fund host, creating legal agreement frameworks and landowner agreement templates, and building stage payment and reporting systems. Social Investment Scotland are now providing support on fund structuring and compliance. By proactively developing this enabling infrastructure, FMS plan to launch a transformational funding vehicle for improving Scotland's river catchments at scale.

Project Pipeline: Learning Points

The FIRNS programme has generated valuable insights about developing Scotland's natural capital project pipeline. Key learnings fall into several themes:

Project Development

- Project development timelines are often longer than anticipated, particularly for early-stage engagement and baseline assessments

- There's a need to balance scientific rigour with practical implementation - "good enough" approaches using proxy measures may be more viable than complex scientific analysis

- Specialist expertise is essential but expensive, creating barriers particularly for smaller projects

- Early demonstration of practical benefits helps maintain stakeholder momentum while developing broader plans

Market Development

- Pure nature markets are unlikely to generate sufficient investment alone, especially in the short term - blended funding approaches are typically needed

- Regional approaches linking nature markets to wider economic opportunities show promise

- Standardisation of approaches (like monitoring frameworks) across diverse projects remains challenging

Community and Landowner Engagement

- Local knowledge is invaluable for identifying practical interventions

- Building trust takes time but is essential for project success

- Community benefits need to be clearly defined and delivered early

- Landowners need clarity on implications for agricultural payments and tax treatment

Project Pipeline: What Would Help

Improving the pipeline of investable projects requires addressing key barriers through:

Aggregation and Scale

- Support regional partnerships and landscape-scale initiatives to achieve investable scale

- Enable project clustering through Regional Land Use Partnerships

- Develop standardised approaches to reduce transaction costs

- Create collaborative platforms to pool smaller projects

Process and Guidance Support

- Provide clear frameworks for project development

- Create template contracts and reporting frameworks

- Develop efficient processes for statutory approvals

- Offer practical tools and how-to guides

Funding and Support

- Offer flexible early-stage funding for project development

- Support baseline assessments and capacity building

- Enable access to specialist expertise

- Maintain knowledge-sharing platforms like the FIRNS Community of Practice

Multi-faceted support and ongoing collaboration between the public sector, project developers, investors, and communities are essential to cultivate a strong pipeline of high-quality, investable projects aligned with Scotland's nature restoration and community benefit goals.

Business Models

The pipeline challenges identified - from scale requirements to development timelines - fundamentally shape how business models must be structured to achieve success. Projects are adapting their financial approaches to address these constraints while maintaining viability

Overview of Business Models in Natural Capital Projects

Natural capital projects typically combine multiple revenue streams and financing sources to achieve viability. Understanding these core elements of the business models such as Revenue, Costs and financing are essential for developing sustainable business models.

Core Revenue Streams

The primary revenue streams for natural capital projects in Scotland currently come from:

- Carbon Credits: Through established mechanisms like the Woodland Carbon Code and Peatland Code. While prices achieved in Scotland after typically higher than global averages this income often requires combining with other revenue streams to achieve project viability.

- Ecosystem Services Payments: Including:

- Natural flood management benefits

- Water quality improvements

- Biodiversity enhancement

- Recreation and tourism income

Cost Structures

Natural capital projects typically face three main categories of costs:

- Development Costs: Including baseline surveys, stakeholder engagement, technical design, and verification/certification costs. FIRNS projects report these being significantly higher than initially estimated.

- Capital Costs: The upfront investment in physical works like tree planting, peatland restoration, or water flow management works. These may benefit from blended finance solutions combining public grants and private investment.

- Operational Costs: Ongoing management, monitoring, and maintenance costs which must be factored into long-term business models and supported by ongoing revenue streams.

Financing Approaches

Projects are typically financed through a combination of:

- Public Grants: Often covering 50-70% of capital costs, particularly for peatland projects supported by the Peatland Action programme.

- Private Investment: Through:

- Direct equity investment

- Debt financing

- Revenue share agreements

- Carbon Credit Pre-sales: Though careful consideration is needed regarding the split between upfront sales and retained credits

Stacking and Bundling

These represent two main approaches to combining revenue streams:

- Stacking: Generating separate revenue streams from different ecosystem services on the same land (e.g., carbon credits plus biodiversity payments)

- Bundling: Packaging multiple benefits into a single product (e.g., premium carbon credits with verified biodiversity and community benefits)

Current market codes generally restrict full stacking of benefits, requiring clear additionality for each revenue stream. This highlights the importance of careful business model design that aligns with market requirements while maximising sustainable revenue opportunities.

Reflections from FIRNS Projects

The FIRNS projects have provided valuable insights into the practical challenges and opportunities around developing viable business models for natural capital projects in Scotland. Key learnings include:

Early Stage Funding Needs and Solutions

FIRNS projects consistently reported underestimating the time and costs involved in the early stages of project development. Activities like community engagement, baseline surveys, and developing governance structures often took significantly longer than anticipated. This highlights a critical need for patient, flexible early-stage funding to support these essential foundations for successful projects.

Potential solutions raised by projects include:

- Dedicating a portion of grant funding specifically for these early-stage activities

- Exploring philanthropic funding or patient capital options

- Collaborating with local partners and networks to share costs and resources

Valuing and Pricing Ecosystem Services

Projects found challenges in robustly quantifying and valuing the full range of ecosystem services their projects could deliver, particularly for benefits beyond carbon like flood management, water quality, and biodiversity. This was compounded by uncertainty around long-term revenues from these sources.

However, projects also saw growing awareness and interest from buyers in these wider benefits. Key needs identified include:

- Developing standardised metrics and methodologies for quantifying co-benefits

- Agreeing clear, long-term payment mechanisms for a wider range of ecosystem services

- Continued engagement with buyers to understand their needs and priorities

Experiences with Different Revenue Models

The most established revenue streams came from woodland creation and peatland restoration via the Woodland Carbon Code and Peatland Code. However, the current carbon price was often seen as insufficient as the sole revenue source.

Projects are therefore exploring innovative approaches like bundling co-benefits with carbon credits, working with local beneficiaries (e.g. insurance companies for flood benefits), and collaborating with other landowners to achieve scale and cost-efficiencies.

Several projects also highlighted the importance of tailored revenue models suited to local contexts and community needs – for example, working with local businesses on nature-based tourism opportunities.

Approaches to Blending Public-Private Finance

Developing an optimal blend of public grants and private investment was a key focus for many projects. Most were combining capital grants (often 50-70% for peatland projects) with revenue-based private finance – through mechanisms like selling a proportion of carbon credits, or via profit-share arrangements.

Getting the right balance and timing of different funding sources was complex – in particular, the interaction between eligibility for public grants and evidence of private finance commitments. Several projects reported challenges due to mismatches between the pace of securing grants vs private investment, with delays in one impacting the other.

There was also debate around the balance of risks and returns between landowners and investors. Some felt that models transferring long-term carbon rights to investors were a poor deal for landowners. Addressing these challenges may require greater flexibility and alignment between public and private funding streams.

Early Lessons on Buyer/Investor Engagement

Effective engagement with buyers and investors was consistently identified as essential, but also an area where projects often underestimated the time and specialist skills required. Particular challenges included:

- Navigating the different needs and priorities of buyers

- Securing clear commitments and pricing from buyers

- Communicating the investment opportunity and structuring deals with investors

Some success factors projects identified include:

- Dedicating sufficient resources to this engagement from an early stage

- Leveraging the experience and connections of expert advisors and platforms like FIRNS and the Community of Practice (as well as the Social Investment Scotland’s wider support networks), Scottish Nature Finance Pioneers, the Ecosystem Knowledge Network and the Green Finance Institute.

- Developing clear, compelling investment propositions backed by robust evidence and data

- Building long-term relationships with aligned investors and buyers

The Flow Country Partnership Case Study

The Flow Country Partnership case study provides practical insights into developing viable business models for peatland restoration at scale.

Flow Country Partnership

Overview of the Project

The Flow Country Partnership is a community-based initiative working to restore degraded peatlands across the Flow Country landscape in Caithness and Sutherland, Scotland. The Flow Country contains globally significant blanket bog, much of which has been damaged by historic drainage and forestry. The partnership aims to restore the peatlands while increasing resilience and opportunities for local communities. Key partners include NatureScot, The Highland Council, RSPB Scotland, the Environmental Research Institute, HIE, and North Highland Initiative.

Project Business Model

Partnership SCIO with a trading subsidiary (Flow Country Restoration Ltd) that will deliver the peatland restoration and hold the carbon assets. This structure allows funds to flow back to the central charity to support running costs and wider community initiatives. The partnership is currently seeking £1-2 million over a 5-year period to build core capacity, expand its project pipeline and unlock its long-term potential.

Key Project Challenges

- Lack of dedicated core staff and leadership to drive things forward at the necessary pace. Much of the work to date has been done 'side of desk' by partner organisations.

- Uncertainty and evolution of carbon and ecosystem markets makes it challenging to build viable long-term business models and attract private investment.

- Potential exclusion of smaller landowners and common grazing if Peatland Action's matched funding requirements favour larger and wealthier landowners.

- The long lag time between initial development and seeing revenue from the sale of carbon units makes early-stage funding difficult.

- Key Project Successes

- Establishment of a dedicated partnership with a suitable governance structure following extensive community consultation.

- Strong collaborative approach and engagement of local contractors and communities.

- Bridging loan provided by Social Investment Scotland, bridging funding gaps and supporting peatland restoration.

- Two initial restoration projects with Peatland Action funding confirmed and a pioneering common grazing scheme under development.

Looking ahead

The Flow Country Partnership has laid the groundwork for landscape-scale peatland restoration driven by community partnerships. With two initial projects underway and a pioneering common grazing scheme in development, the partnership demonstrates how blended finance models can support climate, biodiversity and community outcomes. Over the next 1-2 years, the partnership will focus on building its core team, expanding the project pipeline (particularly on common grazing and smaller landholdings), securing strategic buyers for carbon credits, deepening community engagement, and maximising the biodiversity and community benefits of peatland restoration.

Business Models: Lessons Learned

Project development has revealed several valuable insights.

- Significant upfront funding and time (for up to 2-3 years) is needed before partnerships can hope to generate meaningful revenue from carbon sales or other ecosystem services. Much of this early-stage development work is high risk and may require grant funding.

- Engagement and consultation with local communities is critical but should be balanced with the need for a smaller 'core' team who can get on with delivery and decision making.

- Successful restoration partnerships require a wide range of expertise and capacity covering ecology, project management, grant funding, contracting, stakeholder engagement, communications and business planning.

- Dedicated core staff and leadership are essential to drive complex, multi-stakeholder partnerships forward. Partner organisations can provide valuable expertise but for core function reliance can lead to capacity delays and missed opportunities.

- Effective knowledge sharing between projects can help avoid 're-inventing the wheel' and ensure that lessons learned, and best practice spreads quickly.

Business models: What Would Help

Based on FIRNS project experiences and market analysis, several targeted interventions could help develop more viable business models for natural capital projects:

Market Development Support

- Develop mechanisms like price floors or guaranteed offtake agreements to provide revenue certainty

- Support development of new markets beyond carbon (e.g., biodiversity, water quality)

- Create frameworks for stacking multiple revenue streams where appropriate

- Explore innovative financing mechanisms such as blended finance funds, revolving credit facilities, and revenue support mechanism such as contracts for difference or outcome payments.

Early-Stage Project Support

- Provide dedicated funding for project development activities including baseline assessments and stakeholder engagement

- Support development of robust financial models and business cases

- Enable access to specialist expertise and technical assistance

- Create mechanisms for sharing development costs across multiple projects

Grant and Investment Integration

- Better align public funding timelines with private investment cycles

- Develop more flexible grant structures that support blended finance approaches

- Create clear frameworks for combining different funding sources

- Review intervention rates to ensure accessibility for different project types

Business Model Innovation

- Support further development of approaches like aggregation vehicles and cooperative models

- Continue to support standardised approaches to reduce transaction costs

- Further enable knowledge sharing of successful business models, providing guidance on optimal structures for different project types and scales

These interventions would help address key barriers while maintaining environmental integrity and supporting development of sustainable business models aligned with Scotland's principles for responsible investment in natural capital.

Legal Structures, Governance and Community Benefits

Overview of Legal Structures, Governance and Community Benefits

While business models focus on financial viability, their successful implementation depends on appropriate legal structures and governance. These frameworks must protect stakeholder interests while enabling effective project delivery. Therefore, the development of Scotland's natural capital markets requires robust legal and governance structures that can effectively balance multiple stakeholder interests while delivering environmental and community benefits. These structures must support complex transactions, manage long-term commitments, protect community interests, and provide confidence to investors - all while remaining practical and accessible for land managers and project developers.

FIRNS has provided valuable insights into the range of organisational structures being evolved across Scotland's emerging natural capital sector. Analysis of FIRNS applications shows constituted organisations (including registered charities and trusts) make up 46% of funded projects, while private organisations account for 37% and public bodies the remaining 17%. This diversity reflects the varied approaches being explored, from community-led initiatives to private sector projects and public-private partnerships. Notably, constituted organisations were disproportionately successful in securing funding, making up just 36% of applicants but 46% of grantees, suggesting their governance models may be particularly well-suited to delivering high-integrity natural capital projects.

Figure 7

Click for a full description

Funded FIRNS Projects by Legal Structure - constituted charity or trust-based organisation, constituted community group, public body, private individual or company, academic institution or CIC/community benefit company.

The legal and governance challenges these projects face are significant. They must navigate issues around land tenure, community rights, long-term environmental commitments, and fair distribution of benefits. Many projects are breaking new ground - testing innovative models like farmer cooperatives, community joint ventures, and aggregation vehicles that could enable smaller landholdings to participate in markets. Their experiences offer crucial learning for Scotland's emerging natural capital framework.

Getting these structures right is vital for Scotland's natural capital market development. Effective models are needed to unlock private investment while ensuring projects deliver genuine environmental improvements and community benefits in line with Scotland's principles for responsible investment in natural capital. Without appropriate legal and governance frameworks, projects may struggle to secure investment, manage risks effectively, or maintain community support - all essential elements for building a high-integrity market at scale.

Reflections from FIRNS Projects

Drawing from discussions at the FIRNS Community of Practice event and project experiences, several key themes have emerged around legal and governance structures:

Barriers to Land Manager Participation

Risk, lack of clarity, and financial uncertainty are the primary factors holding back landowners. Many landowners express interest in restoration but hesitate due to the long-term commitments required. With markets not yet established and few success stories to build confidence, committing land to effectively unchangeable uses for extended periods appears too risky. This is particularly acute for farmers operating on marginal profitability. The recent agricultural payments update has not provided sufficient incentives for change, making the status quo appear safer despite interest in restoration approaches.

Supporting Smaller Landholdings

Initial evidence suggests cooperative and catchment-based approaches promise to enable smaller landholding participation. However, these require careful consideration of governance structures and benefit-sharing arrangements.

Legal Models and Governance

Experience from projects like Highland Rewilding suggests simpler legal structures can be effective, particularly for smaller initiatives. Their approach uses basic contracts for micro-businesses that satisfy both landowner and business needs without creating unnecessary complexity. However, there is a demand for a clearer set of template governance models that align with different project types and codes.

Community Stakeholder Perspectives

Key issues raised by communities include:

- The challenge of defining community benefit - with local perspectives often differing from standardised definitions

- The time required to develop genuine community relationships and engagement

- The importance of building circular economies within communities through skill-sharing and strengthening local relationships

- The need for governance structures that enable long-term community participation

The Certification Mark for UK Natural Capital Projects and Dreel Burn Case Studies

The two case studies demonstrate emerging approaches to governance and community benefit delivery - one developing market infrastructure standards, and another showing community-led restoration in practice.

Community Benefits Certification Mark for UK Natural Capital Projects

The Community Inclusion Standard is a nature markets infrastructure project, developed through FIRNS, to establish an aligned approach for community engagement and the potential delivery and verification of measurable social impacts and community benefits from “natural capital” projects across the UK.

The project is led by Deciding Matters, with the Nature Finance Certification Alliance (NFCA) hosting the standard. The NFCA is the UK’s independent industry body for nature markets infrastructure, with membership of over 40 organisations.

The NFCA is championing holistic approaches to natural capital project development and the use of plain English guidance, to reduce the perceived complexity of UK nature markets by the corporate sector, and indeed all market participants.

The standard is designed to be adopted and integrated into ecosystem-service specific UK nature crediting schemes as well into project development best practice for all natural capital projects.

How it works

The standard provide assurance on how natural capital projects engage/include communities, deliver wider social impacts, and deliver community benefits.

Working alongside existing nature crediting schemes, like the Woodland Carbon Code, Peatland Code, Wilder Carbon Standard for Nature and Climate and the UK Carbon Code of Conduct (known as “the Codes”).

Rather than creating separate certification infrastructure, the project aims to open-source it’s standard, for integration into the Codes. Integration of the NFCA standard into a Code, will support it’s compliance with the British Standards Institution (BSI) Nature Markets Framework; in particular with BSI flex 705: Community participation and community benefits.

This promotes alignment and a reduction in current market infrastructure complexity – a known barrier to private sector investment into UK natural capital projects.

The standard will allow the Codes to develop three levels of Community Inclusion Standard certification linked to their credits.

The technical certification standard is supported by a plain English Best Practice Guide, including detailed guidance on the delivery of Community Benefits, as defined within the Scottish Governments’ Natural Capital Market Framework.

Alongside it’s use within the nature markets, it also provides project developers involved in any nature restoration projects (regardless of how they are funded), across the UK, a ‘one-stop-shop’ for guidance on this important topic area.

Allowing projects to demonstrate their high-integrity approach through either self-verification or third-party verification depending on project maturity. The intellectual property for the standard is held by Fife Coast & Countryside Trust (FCCT) in its capacity as co-host of the Nature Finance Certification Alliance (NFCA).

Key Project Challenges

- Balancing robust standards without adding unnecessary bureaucracy

- Addressing proportionality for projects of different scales and types

- Managing high costs of auditing, particularly in remote areas

- Creating a financially viable value proposition for certification

- Ensuring accessibility for smaller and community-led projects

Key Successes

- Strong support from “the codes”, including Woodland Carbon Code and Peatland Code

- Early adoption of principles by market participants

- Development of practical guidance for project developers

- Recognition that effective community engagement reduces delivery risks

- Strong alignment with Scottish Government policy objectives

Looking Ahead

The project continues its work on dovetailing with the BSI standards framework to provide a unified approach to community engagement for effective delivery of social impacts and community benefits across UK natural capital markets.

Future work focuses on:

- Concluding trial audits on three Scottish pilot sites, by project partner Soil Association Certification, and identifying further piloting opportunities in England, Wales and Northern Ireland.

- Digitising the integrated certification processes, with support from project partner, Kana Earth, to assist with adoption and practical implementation.

- Developing training and capacity building components within Scotland, to realise nature markets opportunities for communities. With support from project partners, Scottish Land Commission, Community Land Scotland and Foundation Scotland (the “Natural Capital Partnership Project”)

- Establishing the standard's role in future compliance markets

Case Study: Dreel Burn Investment Readiness Project

The Dreel Burn Investment Readiness Partnership is a community-driven and holistic approach to catchment-scale nature restoration, blending finances from public, philanthropic and private sources to achieve common goals.

Led by Fife Coast and Countryside Trust (FCCT), the project aims to transform the Dreel Burn from a degraded waterway into a clean, biodiverse river system that benefits nature, farmers and local communities.

The project is notable for its highly collaborative approach, bringing together multiple stakeholders including community groups, landowners, local authorities, and environmental organisations, to co-design solutions. With a focus on knowledge transfer to community leaders, building local skills and capacity for the long-term.

Project Development Challenges

- Working with over 30 landowners and stakeholder organisations over a catchment area of c 4,000 hectares.

- Holistic approach requires input from a wide range of experts, while balancing the need for adopting practical "first principles" for timely implementation.

- Developing viable blended finance approaches and nature restoration plans that work for high-value agricultural land.

Project Successes

- Supporting a variety of market infrastructure and nature-based solution innovations, including capture of pollutants with Mycorrhizal fungi, bio-acoustic monitoring, LIDAR-based water pathway analysis, the Ecosystem Restoration Code and the UK Carbon Code of Conduct.

- Built strong working relationships between the community, landowners and environmental organisations through effective governance structure.

- Community empowerment, by enabling leaders to learn about carbon markets, water metrics and playing pivotal role in the project.

- Achieved strong community engagement through regular community education and science activities, playing an exemplary role in the development of the FIRNS funded Community inclusion Standard project, as one of three test audit sites.

Looking Ahead

The Dreel Burn project demonstrates how community benefits and blended finance can work effectively in productive agricultural landscapes through a co-design approach and pragmatic implementation.

The project team is now working to scale this approach across Fife through "Nature Finance Fife" as a regional coordination mechanism.

This includes integrating agricultural payments with carbon credits and supply-chain investments, exploring farming cooperative models to aggregate environmental benefits across catchments. Enabling closer co-ordination between farmers and Fife council programmes and priorities, such as Fife Climate Forest and Food 4 Fife.

The project offers valuable lessons for developing natural capital markets in Scotland, particularly around balancing agricultural productivity with environmental improvements.

Its experiences in supporting innovation while maintaining integrity, and building effective partnerships between diverse stakeholders, provide important insights for similar initiatives.

Legal Structures, Governance and Community Benefits: Learning Points

The experience of FIRNS projects has highlighted several key learnings about effective legal and governance structures for natural capital projects:

- Revenue Streams Are Essential. Without clear, reliable revenue streams, even interested landowners struggle to justify participation. The most successful approaches blend different funding sources and provide certainty around long-term income, particularly important given the extended commitments required for nature restoration.

- Simple Structures Work Best. While projects are complex, simpler legal and governance structures often prove more effective. Overly complicated arrangements can deter participation and increase costs. Basic contracts have worked well for smaller initiatives, particularly when focused on specific outcomes.

- Community Engagement Takes Time. Building genuine community relationships requires significant upfront investment but pays dividends in project success. Early engagement helps shape appropriate governance structures and benefit-sharing arrangements, though this needs to be balanced against project development timelines.

- Scale Through Cooperation. Individual projects often lack the scale needed for market viability, but cooperative approaches show promise. These need careful consideration of governance arrangements to balance different stakeholder interests.

Legal Structures, Governance and Community Benefits: What Would Help

Based on FIRNS project experiences, several interventions could accelerate market development:

Funding and Policy Support

- More flexible funding to support early-stage project development to ensure structures are correct and community is involved

- Clear policy frameworks around long-term land use commitments

Legal and Governance Templates

- Development of model governance structures for different project types

- Template contracts that align with existing codes and standards

- Clarity around community benefit definitions and requirements and guidance on cooperative and aggregation models

Capacity Building Support

- Education and training for landowners on natural capital opportunities

- Support for community engagement and relationship building

- Shared learning from successful projects

- Technical assistance on governance and legal structures

These interventions would help build market confidence while ensuring projects deliver genuine environmental and community benefits aligned with Scotland's principles for responsible investment in natural capital.

Conclusion and Key Learning Points

The FIRNS programme has provided valuable progress and insights into the development of Scotland's natural capital markets. Through supporting 35 projects, a growing market has been further established, and a clearer understanding has emerged about what's needed to continue to scale high-integrity nature restoration with private investment in Scotland. FIRNS has become an integral and vital part of the current pipeline of projects supporting a wide range of capacity building and market innovations.

Market Development Themes

Four key themes emerge across demand, pipeline development, business models, and governance:

- Demand

- Carbon remains dominant revenue model, but other revenue streams are often required to support a viable project

- Significant potential in emerging markets (biodiversity, water quality, natural flood management) which can be further supported by developing policy frameworks

- Buyers often seek local projects where there can be geographic misalignment with supply

- Premium pricing for high-integrity project and credits is possible but also challenging

- Project Pipeline

- Early-stage development typically requires 2-3 years and funding support; grant funding or blended finance is essential for many projects

- Upfront costs (baseline assessments, stakeholder engagement) often underestimated

- Need for patient capital and flexible funding structures

- Business Models

- Multiple revenue streams needed beyond carbon and business models need to reflect this

- Cooperative and landscape-scale approaches show promise

- Patient capital can be essential to support extended development periods

- Technical business modelling support is often required to support projects engaging with buyers

- Legal Structures, Governance and Community Benefits

- Simple governance and legal structures can often be most effective; sharing of models and contracts supports market development

- Community engagement crucial but requires significant time investment

- New frameworks are emerging for benefit sharing and demonstrating community benefits

- Cooperative models show promise for smaller landholdings

Priority Actions for Market Development

Based on FIRNS experience, three immediate priorities emerge:

- Policy Framework Development

- Clear policy guidance on carbon and biodiversity credits, including SBTI compliance for peatland credits, standardised verification processes, and development of a Scottish biodiversity net gain and planning framework

- Support for compliance markets in areas like Biodiversity Net Gain where possible

- Templates for legal structures and community benefit sharing

- Financial Support Evolution

- Flexible early-stage funding

- Better alignment of public and private funding cycles

- Support for aggregation approaches

- Capacity Building

- Knowledge sharing through Communities of Practice

- Technical assistance on business models and governance

- Support for community engagement

The FIRNS programme demonstrates significant potential for scaling private investment in Scotland's nature restoration. Success will require continued collaboration between the public sector, project developers, investors, and communities to build high-integrity markets that deliver genuine environmental and social benefits.

{kind=link}