Green Infrastructure Audit and Compliance Guidance

Purpose

This guidance document sets out to communicate the standards set out within EU Regulations that apply to the Green Infrastructure Fund and how the Lead Partner and grantees will comply with these articles. This guidance also sets out the basic audit framework which the Green Infrastructure Fund will be subject to in order to ensure compliance with these regulations and articles.

The requirements for managing an ERDF Fund can be onerous, applicant guidance has been made available and it provides assistance and information to deliver successful projects which is aligned to EU Regulations and National Rules.

In addition to outlining the audit requirements for the Green Infrastructure Fund, this guidance provides information and assistance regarding the Management and Administration requirements for an ERDF Fund and considers how to:

- Implement good practice

- Set up systems and processes which are easy to use

- Keep a close eye on how the Project is delivering

- Ensure that the Project is managed proactively and issues are addressed.

The following sets out the articles contained within Regulation 1303/2013 of the Official Journal of the European Union:

Article 4(8) – General Principles

The Commission and the Member States shall respect the principle of financial management in accordance with Article 30 of the Financial Regulation.

Article 72 – Management and Control Systems

(a) – Provide a description of the functions of each body involved in management and control, and the allocation of functions within each body;

(b) – Provide compliance with the principle of separation of functions between and within such bodies;

(c) – Provide for procedures for ensuring the correctness and regularity of expenditure declared;

(d) – Provide computerised systems for accounting, for the storage and transmission of financial data and data on indicators, for monitoring and reporting;

(e) – Provide systems for reporting and monitoring where the body responsible entrusts execution of tasks to another body;

(f) – Provide for arrangements for auditing the functioning of the management and control systems;

(g) – Provide for systems and procedures to ensure an adequate audit trail;

(h) – Provide for the prevention, detection and correction of irregularities, including fraud, and the recovery of amounts unduly paid, together with any interest on late payments.

The EU Financial Regulations set out the principles of sound financial management as follows:

Article 30 – Principles of Economy, Efficiency and Effectiveness

(2) i – The principle of economy requires that resources used by the institution in the pursuit of its activities shall be made available in due time, in appropriate quantity and quality and at the best price;

(2) ii – The principle of efficiency concerns the best relationship between resources employed and results achieved;

(2) iii – The principle of effectiveness concerns the attainment of the specific objectives set and the achievement of the intended results.

Background

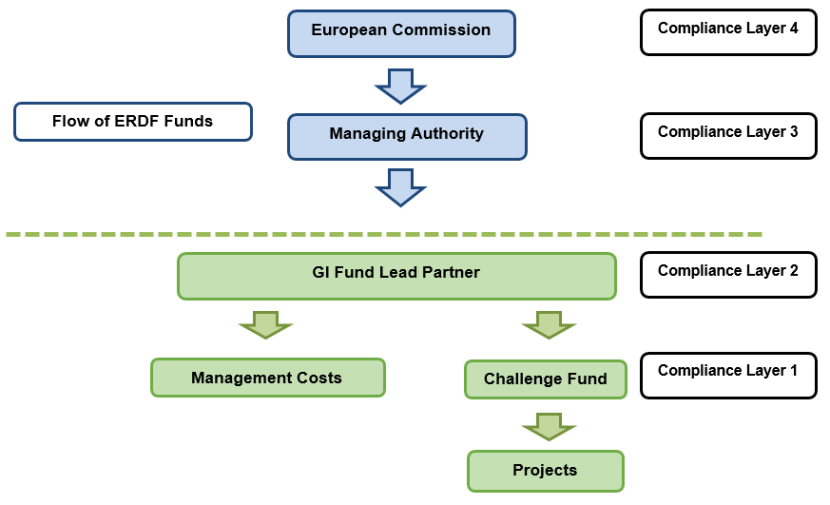

Due to the inherent risks that onerous ERDF funding compliance brings, along with the scale of projects and the structure of the delivery model, a robust governance and control framework is required if the outcomes are to be successfully delivered in a compliant manner.

The following, in Figure 1 below, illustrates the delivery model and indicates at a basic level the layers of audit and compliance.

Fig 1 – Green Infrastructure Fund Delivery Model

Each control layer will bring differing levels of audit and compliance and will be subject to either internal or external audits or both.

Overview – Audit, Compliance & Monitoring

Audit, Compliance and Monitoring will be carried out to ensure the projects are progressing as they should be and that the Green Infrastructure Fund achieves its target outcomes in a compliant manner. Both the Audit & Compliance Plan and the Monitoring & Evaluation Plan will be the primary tools to monitor performance and compliance of the Green Infrastructure Fund. These will allow the following:

- Assess performance and progress

- Maintain financial performance using Budgets and Reforecasts as the primary controls

- Identify strengths and weaknesses of delivery and implement corrective action

- Compile Interim Progress Reports

- Consider lessons learned

- Demonstrate good governance

- Monitor performance using Performance Indicators

- Identify changes through proactive management

- Set out clear Roles & Responsibilities

- Enable effective communication between Lead Partner and Grantees

- Ensure continual compliance with ERDF Rules and Regulations to minimise disallowance or de-commitment risk

- Effective identification and management of risk.

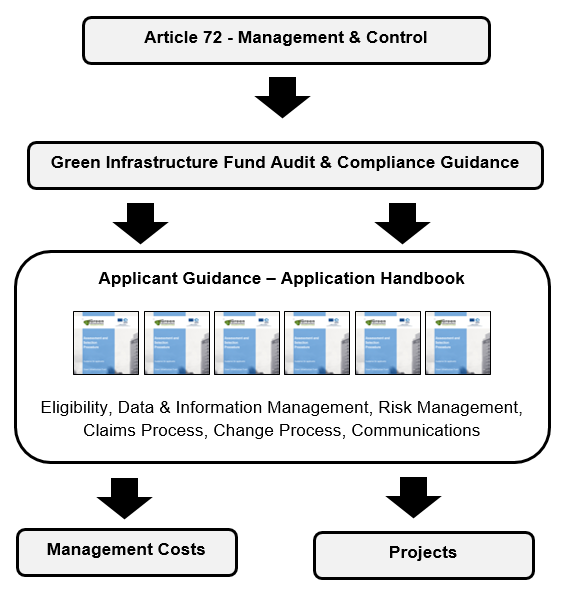

Figure 2 below illustrates how the Audit and Compliance Plan fits into the Delivery Model Governance.

Fig 2 – The Role of Audit & Compliance Guidance

Green Infrastructure Fund, Audit & Compliance Plan

The following provides an outline of the internal audit framework for the Green Infrastructure Fund and relates to the compliance layers 1 and 2 in Figure 1 above.

Scottish Natural Heritage, as Lead Partner, will monitor and review the fund through a number of approaches to ensure a robust control framework is maintained. Findings of audits and compliance checks will be used to measure the performance and governance of the Green Infrastructure Fund and form a basis for recommendations if appropriate. The plan will be primarily driven by the quarterly claims cycle as in Table 1 below:

Table 1 – Green Infrastructure Fund Audit Type & Frequency

|

Audit Type |

Frequency |

|

Risk Based Samples |

Monthly & Quarterly |

|

Compliance Checks |

Quarterly |

|

Performance Measures |

Quarterly |

External Monitoring & Audit Framework

The following provides an outline of the external audit framework for the Green Infrastructure Fund and relates to the compliance layers 3 and 4 in Figure 1 above.

Quarterly Claims

The Scottish Government as the Managing Authority will perform verification checks on the claims submitted through EUMIS by Scottish Natural Heritage as the Lead Partner and is performed on a sample basis of approximately 20%.

Article 125 Pre-Claim Check

This is intended to be a preventative visit by the Scottish Government to identify possible project issues and prevent reoccurrence of problems. This will be ideally conducted within the first 3 months of the Project. This visit offers the opportunity for the Scottish Government as Managing Authority to familiarise themselves with those delivering the Green Infrastructure Fund and assess the monitoring requirements.

Article 125 Progress & Verification Visit

A member of the Scottish Government Structural Funds Division will conduct one or more in-depth monitoring visits during the lifetime of the Project. This will verify the declared expenditure, that the Projects products or services have been delivered in accordance with the Offer Letter and that the Projects claims and activities comply with the European Commission and National Rules.

Article 125 Visit

Each year, a number of Projects will be selected for an in-depth Article 125 inspection. Article 125 audits are undertaken on a sample basis or on a risk based assessment and will be conducted by the Scottish Government Audit Authority Team. This type of audit can last several days. It is important to note that any irregularities identified during an Article 16 visit will result in funds being recovered directly from the Green Infrastructure ERDF grant.

Other Visits

There is also the possibility that the Project will be audited by the European Commission or the European Court of Auditors, both of whom select a sample of projects for scrutiny.

Essential Criteria to Audit & Monitoring Visits

It is essential that key members of staff involved in either Scottish Natural Heritage, as the Lead Partner, or for Projects are available during any Article 125 visits, monitoring visits, in addition to any other audits whether by the Green Infrastructure Fund or external. These should typically be the Project Manager and the person(s) responsible for the Projects financial and claim record keeping.

It is the responsibility of the Offer Letter recipient to have all the relevant documentation available for monitoring or inspection purposes. For the Green Infrastructure Fund, this is Scottish Natural Heritage as the Lead Partner and this is built into the management and control systems to allow for a clear audit trail.

Irregularities

The European Commission definition of an irregularity is given in EC Regulation 1083/2006:

“…any infringement of a provision of Community Law resulting from an act or omission by an economic operator, which has, or would have, the effect of prejudicing the general budget of the Communities by charging an unjustified item of expenditure to the general budget”.

Action will be taken to follow up and correct any irregularity in a timely manner and steps will be taken to ensure the irregularity is not repeated. If any irregularity is identified, funds will be recovered and deducted from the Green Infrastructure ERDF grant. The basis for sharing or assigning disallowance or de-commitment between the Managing Authority, Lead Partner and Grantees will be set out in the Delivery Contracts and Offers of Grant.

Article 72 – Management & Control Systems – Compliance Guidance for projects

The following offers guidance in order to demonstrate compliance with principles of Article 72, which is the under-pinning requirement for the Green Infrastructure Fund for management and control.

Referring to the Green Infrastructure Fund Applicant Guidance will assist in compliance with Article 72.

Management and Control Systems will include but not limited to the following:

- Management Structures

- Suitable Management Information Systems (MIS)

- Financial Systems & Records

- Project Files

- Data & Information Management – Document Retention

- Authorisation Limits

- Separation of Roles & Responsibilities

- Health & Safety

- Equal Opportunities

- VAT Registration & Insurance

- Audit Trail & Verification for Expenditure & Income

- Financial Reporting

- EU Procurement Rules & Regulations

- ERDF Publicity Rules.

The following sets out the requirements of Management and Control Systems for the Green Infrastructure Fund and are provided within the headings of Article 72 principles:

|

Principle (a) – Provide a description of the functions of each body involved in management and control and the allocation of functions within each body. Principle (b) – Provide compliance with the principle of separation of functions between and within such bodies. |

|

|

Principle (c) – Provide for procedures for ensuring the correctness and regularity of expenditure declared. Principle (d) – Provide computerised systems for accounting, for the storage and transmission of financial data and data on indicators, for monitoring and reporting. Principle (g) – Provide for systems and procedures to ensure an adequate audit trail. |

|

|

Principle (e) – Provide systems for reporting and monitoring where the body responsible entrusts execution of tasks to another body. Principle (f) – Provide for arrangements for auditing the functioning of the management and control systems. Principle (h) – Provide for the prevention, detection and correction of irregularities, including fraud, and the recovery of amounts unduly paid, together with any interest on late payments. |

|

As illustrated in Figure 1, the project delivery will be entrusted to grantees. To ensure successful and compliant delivery of projects, Scottish Natural Heritage as Lead Partner has set-up the following legal, monitoring and reporting systems:

|

Audit Timeline

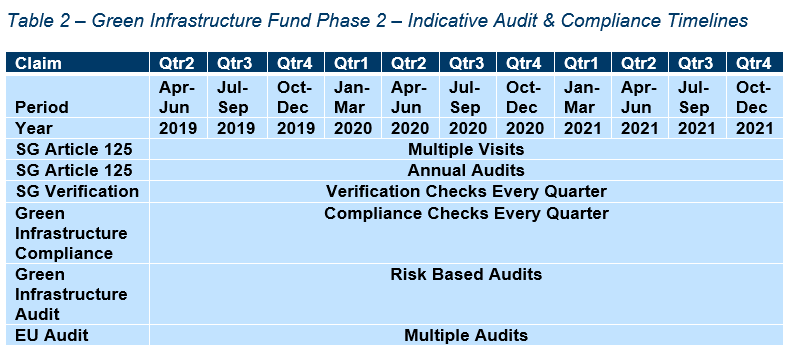

A guide to the audit and compliance timelines for Phase 2 of the Green Infrastructure Fund is given in Table 2 below:

Table 2 – Green Infrastructure Fund Phase 2 – Indicative Audit & Compliance Timelines

Contact

Green Infrastructure